Finance, Money and Climate Change

New research report on green finance and green monetary policy

As fighting climate change becomes the world’s top post-pandemic priority, financial intermediaries, their regulators and central banks have all been called to contribute. A major new research report exploring the scope and limits of green finance and the possibility of ‘greening’ monetary policies will be launched at an online panel discussion hosted by Europe’s leading economic policy journal on Thursday 21 October 2021.

Markus Brunnermeier of Princeton University and CEPR, who has co-authored the study with former top French and international policy-maker Jean-Pierre Landau of Sciences Po, will present a new framework for thinking about finance, money and climate change – identifying the trade-offs and key choices to be made. Among the researchers’ conclusions:

- Climate should be a part of central banks’ risk assessments.

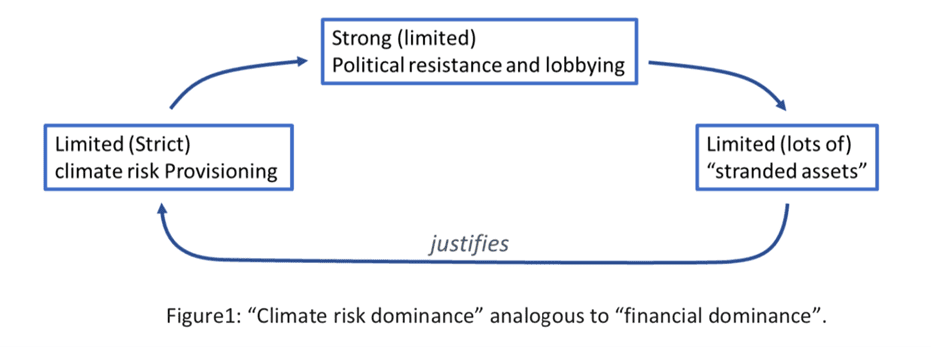

- There may be large quantities of so-called ‘stranded assets’ – those whose value suddenly drops. These losses in value can occur due to climate change directly, but more likely and earlier due to shifts in policy. For example, sites for the extraction of non-renewable sources of energy might turn into stranded assets if energy policy curbs the relevant markets. This, in turn, generates questions about the role of markets for insurance against such transformations, and that of decision-makers in limiting costly policy uncertainty.

- A large fraction of climate risk comes from policy uncertainty. These uncertainties act like a Pigouvian ‘tax’, but unlike textbook Pigouvian taxes, they do not generate revenues and hence are highly inefficient. Bank regulation should take these risks into account.

- There is the possibility of a positive feedback loop between private actions and future policy. If private institutions provision for the impact of future climate policies, they will grow more resilient when measures are taken. In turn, increased preparation in the private sector may make it easier and politically more feasible for public decision-makers to adopt the necessary policies.

- In contrast, in the absence of preparedness of private actors, a ‘climate risk dominance’ phenomenon could arise. In essence, if no provisions are taken, implementing strict climate regulation becomes too risky and costly to undertake.

- There are important questions around who should decide whether a sector or specific asset is ‘green’ or ‘brown’. Ratings of environmental, social and governance (ESG) sustainability are not yet reliable: there is low correlation with each other and low correlation with actual emissions levels.

- Central banks may want to take account of several climate change-related aspects when designing and implementing monetary policies. For example, climate policy initiatives might increase r* – the interest rate at which monetary policy is neither expansionary nor contractionary.

- At the same time, central banks should retain absolute discretion to interrupt any action if their first-priority objective of price stability were to be compromised.

The study notes differences in the climate change challenge facing central banks such as the US Federal Reserve (‘the Fed’) and the European Central Bank (ECB) given differences in their mandates. For example, potential climate-related controversies surround the ECB’s corporate bond purchases as part of its programme of quantitative easing.

More…

In democratic societies, decisions on allocating resources and redistributing incomes are taken by elected bodies. Obviously, policies relating to climate change belong in that category. Independent central banks are non-elected ‘agents’ of society; they have a well-specified mandate to stabilise the economy.

It can be argued that central banks like the Fed and the ECB would be going beyond their mandate if they were to tweak their instruments of monetary policy to allocate resources and direct credit.

The situation may be particularly complex for the ECB. Compared with the Fed, its mandate is both more hierarchical – with price stability as a priority objective – and more complex. The Treaty states that ‘… without prejudice to the objective of price stability’, the Euro system shall also ‘support the general economic policies in the Union with a view to contributing to the achievement of the objectives of the Union’. These include ‘full employment’ and ‘balanced economic growth’.

To the extent that price stability is not compromised, and fighting climate change is a major (recently reaffirmed and emphasised) priority of the EU, the question arises as to whether the ECB can use some of its available instruments to pursue an additional climate change objective. This is certainly a point made by many climate activists.

But this immediately raises further questions. Governments in various countries pursue many policies. Is it legitimate for the central bank to pick and freely select its preferred secondary objective? Or should it defer to elected bodies if the policy aims at allocating public resources, as seems normal in a representative democracy.

The trade-off is real and difficult. On the one hand, if the central bank were to assess the situation itself and contemplate actions, its legitimacy would be challenged. In addition, it would expose itself to various political pressures. On the other hand, if it requests some formal guidance by elected bodies (such as the parliament), it risks fuelling the perception that it has lost its independence.

There might be subtle ways and procedures to navigate between these risks, but the dangers are real and would justify great caution. Under all circumstances, the central bank should keep the absolute discretion to interrupt any action or programme if its first-priority objective – price stability – were to be compromised.

On the European side, the ECB has stated that ‘environmental externalities are best tackled by taxation or tradable permits, but it has already begun to purchase green bonds. Furthermore, tilting asset purchases in favour of ‘green’ assets may be justified by the market neutrality principle.

So far, asset purchase programmes have included large firms that are heavier in emissions, as these industries issue more bonds. Thus, to restore market neutrality, the central bank should buy assets from less polluting industries. Within the market neutrality framework, the ECB can already adapt its asset purchases to support the climate transition.

‘Finance, Money and Climate Change’

Authors:

Markus Brunnermeier (Princeton University)

Jean-Pierre Landau (Sciences Po)